Blog / product

Mortgage Tech is Fundamentally Broken

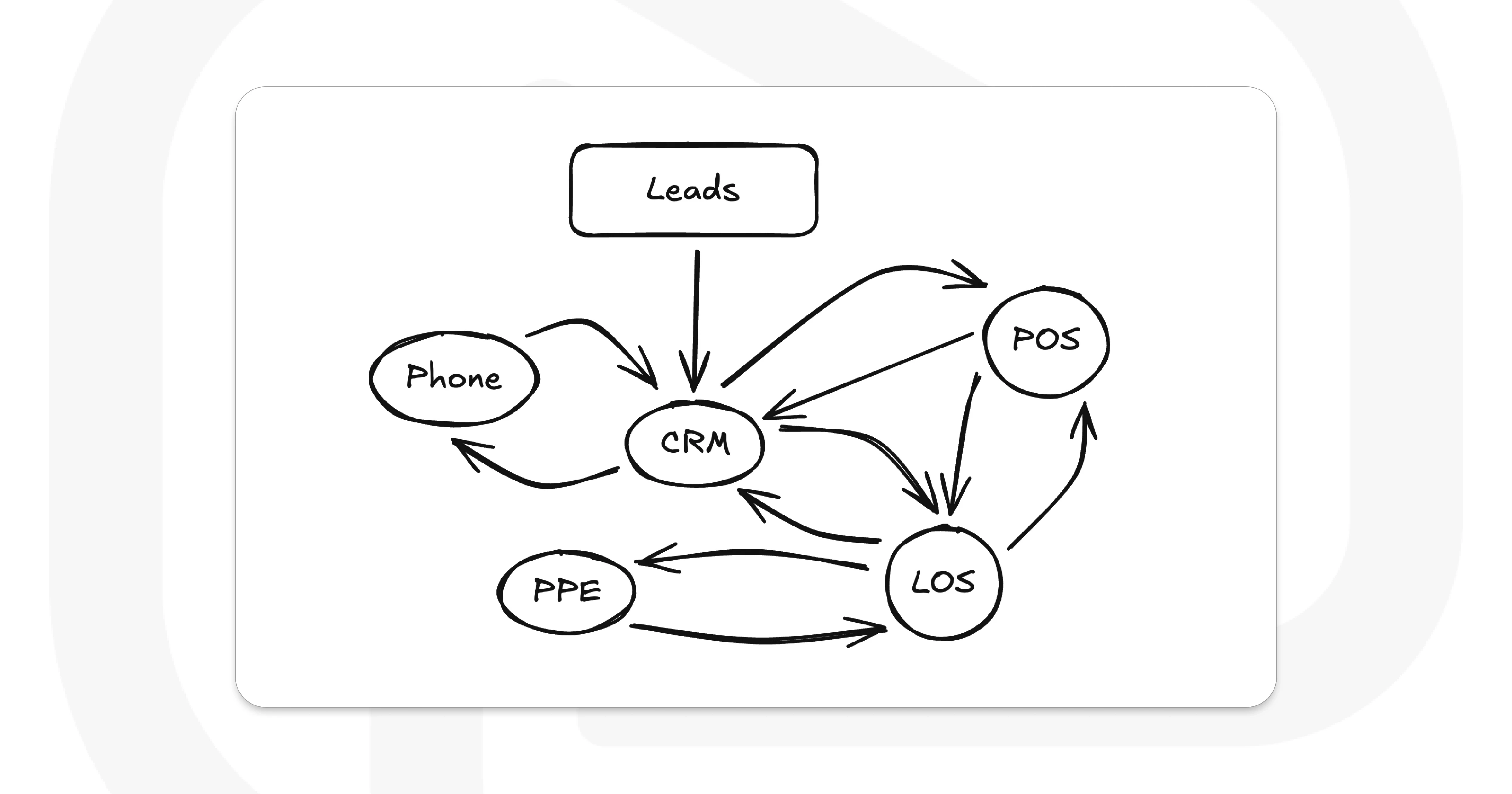

If you work in mortgages, this diagram probably looks familiar.

The arrows between CRM, LOS, POS, PPE, and Phone systems form a maze that every lender, broker, and originator lives inside. You don’t need to be a UX visionary to look at this diagram and see a problem. Yet somewhere along the line, our industry collectively decided this was going to be the standard.

Despite so-called advancements in technology, the cost of loan origination has continued to rise.

The result is an ecosystem that looks more like a patchwork quilt than a platform. Data is siloed, workflows are fragmented, and user experiences are defined by constant context-switching between systems that were never meant to cooperate.

The future of mortgage technology isn’t about connecting systems — it’s about ending the need for them.

The “System of Record” Problem

A CRM that can’t actually manage a customer relationship isn’t really a CRM. Yet that’s what most lenders rely on — a tool that only tracks part of the relationship.

For a loan officer, the customer journey isn’t limited to emails and follow-ups. It includes credit pulls, loan structuring, pricing, locking, document requests, and compliance checks. If the system can’t handle those, then it’s not managing relationships — it’s just tracking them.

The real problem is that the categories themselves — CRM, LOS, POS, PPE — were never meant to be separate. They’re fragments of what should have always been a single system of record.

The Rocket Effect

Only the largest players, like Rocket Mortgage or Loan Depot, have managed to overcome this fragmentation. Their loan officers will have never heard of an LOS, PPE, or POS. It’s one system. But they accomplished this only by building everything internally, supported by massive engineering teams and nine-figure tech budgets.

When top producers leave those environments to start their own shops, they’re stunned by how primitive the available tools are. Pulling credit becomes a multi-step process. Income calculations are done in a spreadsheet. The list goes on.

Meanwhile, Rocket continues gaining market share largely because of its unified platform advantage. Most recently, they boasted 4x higher conversion rates on purchase and refinance applications by launching an AI agent.

Technology isn’t the only differentiator — but it’s the one that scales the fastest.

Why Innovation Stalls

Innovation in mortgage tech has always been constrained by two realities:

1. Regulation and compliance

Deep domain expertise is mandatory just to get started. The cost of error is high, and the margin for experimentation is small. If you’re a talented startup looking to upend an industry, you’ll have an easier time building elsewhere.

2. Closed, slow-moving vendors

The systems required for compliance — credit, AUS, pricing, delivery — are owned by a handful of companies that operate as closed ecosystems. APIs are gated, integrations are expensive, and documentation is often nonexistent.

In most industries, startups innovate by building on top of open platforms. In mortgage, innovation depends on permission from legacy vendors.

Together, these factors deter new entrants and make true modernization nearly impossible.

The Path Forward

At Gizmo, we’re building the operating system for mortgage lenders. We believe the lines between CRM, LOS, POS, and PPE will blur until they disappear entirely.

We’re betting on a future that is:

Unified

Originators will check in to work each morning and log off at night having opened exactly one application. They won’t load an LOS, then a CRM, then a phone system. They won’t need to jump into a PPE for pricing or a POS for e-sign. The entire lifecycle will exist in a single workspace.

Our customers today are already using branded phone, pulling credit, structuring loan applications, and running dual AUS from one platform. Our roadmap is packed with future updates that will continue to consolidate functionality.

Open & Extensible

The most successful systems will encourage innovation, not restrict it. They’ll offer well-documented APIs, SDKs, and self-serve development environments where lenders and partners can build extensions without waiting for vendor approval.

We recently launched our Developer Documentation, with detailed guides, API references, and test suites. We actively maintain TypeScript & Python SDKs, making it easier than ever for developers to build on top of Gizmo.

Constantly Evolving

The next generation of systems won’t wait for annual releases or vendor upgrades.

They’ll evolve continuously — shipping new integrations, AI capabilities, and workflow improvements weekly. Lenders will adopt innovation at their own pace, not on someone else’s release schedule.

AI-First

AI won’t replace the loan originator, but it will redefine their work.

AI agents will pre-qualify leads, structure files, verify data, and manage documents before a human ever touches the file. Human expertise will shift from administration to strategy, and customer experience will improve as a result.

Loan officers using our platform today are converting higher than ever with Outbound AI Agents teeing them up with warm transfers. We’ve begun privately demonstrating our upcoming AI assistant, which can structure loans, process documents, and fix qualifying errors side-by-side with its human counterpart.